what should occur when a projects net present value is determined to be negative?

Defining NPV

Net Nowadays Value (NPV) is the sum of the present values of the cash inflows and outflows.

Learning Objectives

Define Net Present Value

Primal Takeaways

Key Points

- Because of the fourth dimension value of money, greenbacks inflows and outflows simply can be compared at the same point in time.

- NPV discounts each inflow and outflow to the nowadays, and then sums them to meet how the value of the inflows compares to the other.

- A positive NPV means the investment is worthwhile, an NPV of 0 ways the inflows equal the outflows, and a negative NPV means the investment is not skillful for the investor.

Key Terms

- cash inflow: Cash that is received by the investor. For example, dividends paid on a stock owned past the investor is a cash arrival.

- greenbacks outflow: Any cash that is spent or invested by the investor.

Every investment includes cash outflows and cash inflows. There is the cash that is required to make the investment and (hopefully) the return.

In order to meet whether the greenbacks outflows are less than the greenbacks inflows (i.e., the investment earns a positive render), the investor aggregates the cash flows. Since cash flows occur over a period of time, the investor knows that due to the time value of money, each cash flow has a certain value today. Thus, in order to sum the cash inflows and outflows, each cash flow must be discounted to a mutual point in fourth dimension.

Airplane: Before purchasing a new airplane, airlines evaluate the NPV of the programme by calculating the PV of the revenue it tin can earn from it and the PV of its price (e.g., buy cost, maintenance, fuel, etc. ).

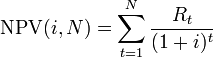

The net present value (NPV) is simply the sum of the nowadays values (PVs) and all the outflows and inflows:

NPV = PVInflows+ PVOutflows

Don't forget that inflows and outflows have opposite signs; outflows are negative.

Also recall that PV is constitute by the formula [latex]\text{PV}=\frac { \text{FV} }{ { (1+\text{i}) }^{ \text{t} } }[/latex] where FV is the futurity value (size of each cash catamenia), i is the discount rate, and t is the number of periods between the nowadays and future. The PV of multiple cash flows is simply the sum of the PVs for each cash flow.

The sign of NPV can explain a lot about whether the investment is good or non:

- NPV > 0: The PV of the inflows is greater than the PV of the outflows. The coin earned on the investment is worth more than today than the costs, therefore, it is a expert investment.

- NPV = 0: The PV of the inflows is equal to the PV of the outflows. At that place is no difference in value between the value of the money earned and the money invested.

- NPV < 0: The PV of the inflows is less than the PV of the outflows. The coin earned on the investment is worth less today than the costs, therefore, it is a bad investment.

Computing the NPV

The NPV is plant by summing the present values of each individual cash flow.

Learning Objectives

Summate a project's Net Present Value.

Key Takeaways

Key Points

- Cash inflows accept a positive sign, while cash outflows are negative.

- To find the NPV accurately, the investor must know the exact size and time of occurrence of each cash menses. This is easy to find for some investments (similar bonds ), merely more than difficult for others (like industrial machinery).

- Investors use different rates for their discount rate such equally using the weighted average cost of majuscule, variable rates, and reinvestment rate.

Key Terms

- discount rate: The interest rate used to disbelieve hereafter cash flows of a financial instrument; the annual interest rate used to decrease the amounts of future cash flow to yield their present value.

- variable: something whose value may be dictated or discovered.

- greenbacks flow: The sum of cash revenues and expenditures over a period of fourth dimension.

Calculating the NPV

The NPV of an investment is calculated by adding the PVs ( present values ) of all of the cash inflows and outflows. Cash inflows (such as coupon payments or the repayment of principal on a bond) accept a positive sign while cash outflows (such as the money used to purchase the investment) take a negative sign.

Net Nowadays Value (NPV) Formula: NPV is the sum of of the present values of all greenbacks flows associated with a project. The business volition receive regular payments, represented by variable R, for a flow of time. This menstruation of time is expressed in variable t. The payments are discounted using a selected interest rate, signified past the i variable.

The accurate calculation of NPV relies on knowing the amount of each cash menstruation and when each volition occur. For securities like bonds, this is an easy requirement to see. The bail clearly states when each coupon payment volition occur, the size of each payment, when the principal volition exist repaid, and the cost of the bond. For other investments, this is not so simple to determine. When a new piece of mechanism is purchased, for example, the investor (the purchasing company) has to estimate the size and occurrence of maintenance costs equally well as the size and occurrence of the revenues generated by the machine.

The other integral input variable for computing NPV is the discount rate. There are many methods for calculating the appropriate discount rate. A firm'due south weighted average cost of majuscule after tax (WACC) is oftentimes used. Since many people believe that it is appropriate to employ college discount rates to adjust for run a risk or other factors, they may choose to use a variable discount rate.

Another approach to selecting the discount rate cistron is to decide the rate that the capital needed for the project could render if invested in an alternative venture. If, for example, the capital required for Project A tin can earn five% elsewhere, use this discount charge per unit in the NPV calculation to let a direct comparing to be made betwixt Project A and the alternative. Related to this concept is to use the firm'southward reinvestment rate. Reinvestment rate can exist defined every bit the charge per unit of return for the firm's investments on boilerplate, which can likewise be used as the discount charge per unit.

Interpreting the NPV

A positive NPV ways the investment makes sense financially, while the reverse is truthful for a negative NPV.

Learning Objectives

Interpret a series of internet nowadays value calculations

Key Takeaways

Central Points

- When inflows exceed outflows and they are discounted to the present, the NPV is positive. The investment adds value for the investor. The opposite is true when NPV is negative.

- A NPV of 0 means in that location is no alter in value from the investment.

- In theory, investors should invest when the NPV is positive and it has the highest NPV of all bachelor investment options.

- In practice, determining NPV depends on being able to accurately determine the inputs, which is difficult.

Primal Terms

- greenbacks flow: The sum of cash revenues and expenditures over a catamenia of time.

The NPV is a metric that is able to determine whether or not an investment opportunity is a smart fiscal decision. NPV is the present value (PV) of all the cash flows (with inflows beingness positive cash flows and outflows being negative), which means that the NPV can be considered a formula for revenues minus costs. If NPV is positive, that means that the value of the revenues (cash inflows) is greater than the costs (cash outflows). When revenues are greater than costs, the investor makes a profit. The contrary is true when the NPV is negative. When the NPV is 0, there is no gain or loss.

In theory, an investor should make whatsoever investment with a positive NPV, which means the investment is making coin. Similarly, an investor should refuse any selection that has a negative NPV because information technology only subtracts from the value. When faced with multiple investment choices, the investor should always choose the pick with the highest NPV. This is only true if the choice with the highest NPV is not negative. If all the investment options take negative NPVs, none should be undertaken.

The decision is rarely that cut and dry, however. The NPV is simply every bit good as the inputs. The NPV depends on knowing the discount charge per unit, when each cash menses volition occur, and the size of each flow. Cash flows may not exist guaranteed in size or when they occur, and the disbelieve rate may be hard to determine. Any inaccuracies and the NPV will be affected, as well.

Mechanism: Being able to accurately observe the NPV of a piece of machinery means having a skillful idea when all costs are going to occur (when it will need fixing) and when it will generate acquirement (when it will be used on a job).

Advantages of the NPV method

NPV is easy to use, easily comparable, and customizable.

Learning Objectives

Describe the advantages of using net present value to evaluate potential investments

Key Takeaways

Central Points

- When NPV is positive, it adds value to the firm. When it is negative, it subtracts value. An investor should never undertake a negative NPV project.

- As long as all options are discounted to the same signal in time, NPV allows for easy comparison betwixt investment options. The investor should undertake the investment with the highest NPV, provided information technology is possible.

- An reward of NPV is that the discount rate can be customized to reflect a number of factors, such as risk in the market.

Key Terms

- gain (or loss): If an investment earns more value than it costs, the divergence is the gain. If it costs more than than it earns, the difference is a loss.

Computing the NPV is a mode investors determine how attractive a potential investment is. Since it substantially determines the present value of the gain or loss of an investment, it is piece of cake to understand and is a swell decision making tool.

When NPV is positive, the investment is worthwhile; On the other hand, when it is negative, information technology should not be undertaken; and when information technology is 0, in that location is no deviation in the present values of the cash outflows and inflows. In theory, an investor should undertake positive NPV investments, and never undertake negative NPV investments. Thus, NPV makes the conclusion making process relatively direct forward.

NPV Decision Table: NPV but and clearly shows whether a project adds value to the firm or non. It's easy of apply in determination making is one of its advantages.

Another advantage of the NPV method is that it allows for easy comparisons of potential investments. As long as the NPV of all options are taken at the same signal in time, the investor can compare the magnitude of each option. When presented with the NPVs of multiple options, the investor volition simply choose the option with the highest NPV considering information technology will provide the about additional value for the firm. However, if none of the options has a positive NPV, the investor will not choose any of them; none of the investments will add value to the house, so the firm is ameliorate off non investing.

Furthermore, NPV is customizable then that it accurately reflects the financial concerns and demands of the house. For example, the discount rate tin be adjusted to reflect things such as risk, opportunity toll, and changing yield curve premiums on long-term debt.

Disadvantages of the NPV method

NPV is hard to gauge accurately, does not fully business relationship for opportunity cost, and does not give a complete flick of an investment'southward gain or loss.

Learning Objectives

Talk over the disadvantages of using the NPV method

Cardinal Takeaways

Key Points

- NPV is based on time to come greenbacks flows and the discount rate, both of which are hard to estimate with 100% accuracy.

- There is an opportunity toll to making an investment which is not built into the NPV calculation.

- Other metrics, such as internal charge per unit of return, are needed to fully determine the gain or loss of an investment.

Key Terms

- Opportunity cost: The cost of an opportunity forgone (and the loss of the benefits that could be received from that opportunity); the almost valuable forgone alternative.

There are a number of disadvantages to NPV. NPV is still unremarkably used, but firms will also use other metrics before making investment decisions.

Medicine: Drug developers must try to calculate the futurity revenues of a drug in order to notice the NPV to make up one's mind if it is worth the cost of development.

The showtime disadvantage is that NPV is only as accurate every bit the inputted information. It requires that the investor know the exact discount rate, the size of each cash flow, and when each cash flow will occur. Oftentimes, this is impossible to determine. For example, when developing a new product, such equally a new medicine, the NPV is based on estimates of costs and revenues. The cost of developing the drug is unknown and the revenues from the sale of the drug can exist hard to estimate, especially many years in the future.

Furthermore, the NPV is merely useful for comparing projects at the same time; it does not fully build in opportunity cost. For example, the day after the visitor makes a decision virtually which investment to undertake based on NPV, information technology may discover there is a new option that offers a superior NPV. Thus, investors don't simply pick the option with the highest NPV; they may pass on all options because they call up another, better, pick may come along in the futurity. NPV does not build in the opportunity toll of not having the uppercase to spend on time to come investment options.

Another issue with relying on NPV is that it does not provide an overall picture of the proceeds or loss of executing a certain project. To see a percentage proceeds relative to the investments for the project, internal rate of return (IRR) or other efficiency measures are used as a complement to NPV.

NPV Profiles

The NPV Profile graphs the human relationship betwixt NPV and discount rates.

Learning Objectives

Draw the human relationship between a project'south disbelieve charge per unit and its Net Nowadays Value

Key Takeaways

Key Points

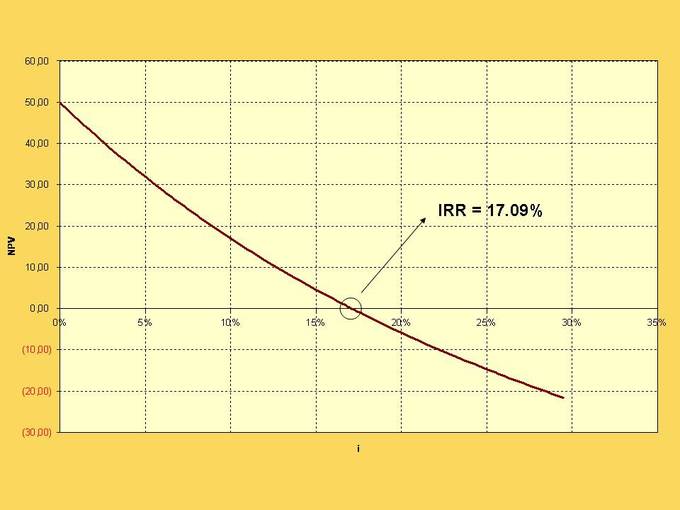

- The NPV Profile is a graph with the discount charge per unit on the x-axis and the NPV of the investment on the y-axis.

- College discount rates mean cash flows that occur sooner are more influential to NPV. Since the earlier payments tend to exist the outflows, the NPV contour by and large shows an inverse relationship between the discount rate and NPV.

- The discount rate at which the NPV equals 0 is chosen the internal charge per unit of render (IRR).

Key Terms

- discount rate: The interest rate used to disbelieve future greenbacks flows of a financial musical instrument; the annual interest charge per unit used to subtract the amounts of future cash flow to yield their present value.

- internal rate of render: IRR. The rate of render on an investment which causes the net present value of all future cash flows to be nix.

NPV Profiles

The NPV calculation involves discounting all cash flows to the nowadays based on an causeless discount rate. When the discount rate is large, there are larger differences between PV and FV (present and future value) for each cash menses than when the discount rate is small. Thus, when discount rates are big, cash flows further in the future affect NPV less than when the rates are small. Conversely, a depression discount rate ways that NPV is affected more than by the cash flows that occur further in the future.

The relationship betwixt NPV and the discount rate used is calculated in a chart called an NPV Profile. The independent variable is the discount charge per unit and the dependent is the NPV. The NPV Profile assumes that all greenbacks flows are discounted at the same rate.

NPV Profile: The NPV Profile graphs how NPV changes every bit the discount rate used changes.

The NPV profile ordinarily shows an inverse relationship between the discount rate and the NPV. While this is non necessarily truthful for all investments, it can happen because outflows generally occur before the inflows. A higher discount rate places more than emphasis on earlier cash flows, which are generally the outflows. When the value of the outflows is greater than the inflows, the NPV is negative.

A special discount rate is highlighted in the IRR, which stands for Internal Charge per unit of Return. Information technology is the discount rate at which the NPV is equal to zero. And it is the discount charge per unit at which the value of the cash inflows equals the value of the cash outflows.

Source: https://courses.lumenlearning.com/boundless-finance/chapter/net-present-value/

0 Response to "what should occur when a projects net present value is determined to be negative?"

Post a Comment